In the State of Open Banking 2023, we take a pulse check of the industry and the opportunities it presents for banks, fintechs, brokers and lenders. In this article, we look into the consumer perspective. Their interest in and the uptake of Open Banking powered services.

Open Banking has enormous potential to offer real value to consumers. Businesses are launching new and innovative use cases, and more are on the horizon. But consumer trust is an important factor that will influence uptake. Consumers are rightfully cautious about sharing financial information, especially with recent high-profile data breaches in the telco and insurance sectors. Also, for years they have heard the message from banks and government to not digitally share their financial information using insecure methods such as screen scraping.

All this makes education on the benefits of Open Banking critical to building consumer trust. It’s a challenge and an opportunity, as consumers value security, privacy, control and transparency – exactly what Open Banking offers. In fact, consumer attitudes show that the benefits Open Banking offers are appealing to many consumers, especially younger generations.

How do we know all of this? We asked. Earlier this year, we surveyed 1,066 Australians from all walks of life about financial data sharing, potential use cases, the things they find important when sharing their data and who they trust with it.

Key insights from our consumer research

Our research revealed that consumers want the benefits Open Banking will bring. While they remain concerned about their data getting stolen, sold, or misused, this sentiment validates that Open Banking has real value for consumers as an alternative to unsafe practices they’ve been warned against. Educating consumers about this is essential.

Here are our top 4 insights about consumer attitudes.

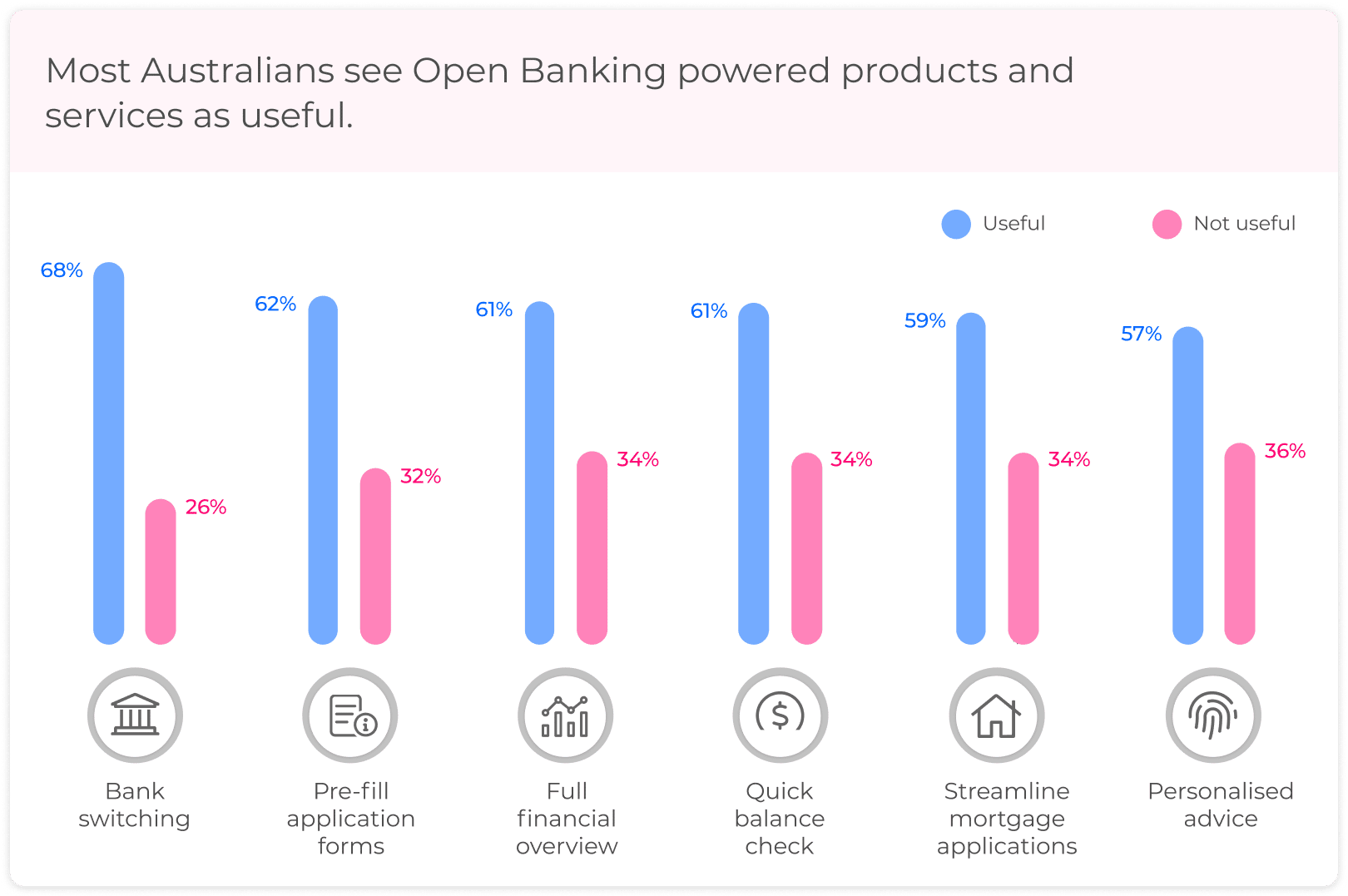

1. Australians value Open Banking powered products and services

We presented Australian consumers with six potential Open Banking use cases:

- full financial overviews

- streamlined mortgage applications

- pre-fill application forms

- quick balance checks

- direct debit and payee switching

- personalised advice.

When asked if they would find these useful, the answer was clear: yes, Australians see the benefits of what Open Banking can offer.

- 57% of Australians see value in many Open Banking use cases

- 58% think linking their bank account to share financial data and get access to personalised products and services is useful

- 68% of respondents say they would find it useful to use Open Banking to switch over payee and direct debit details to a new bank (the top result).

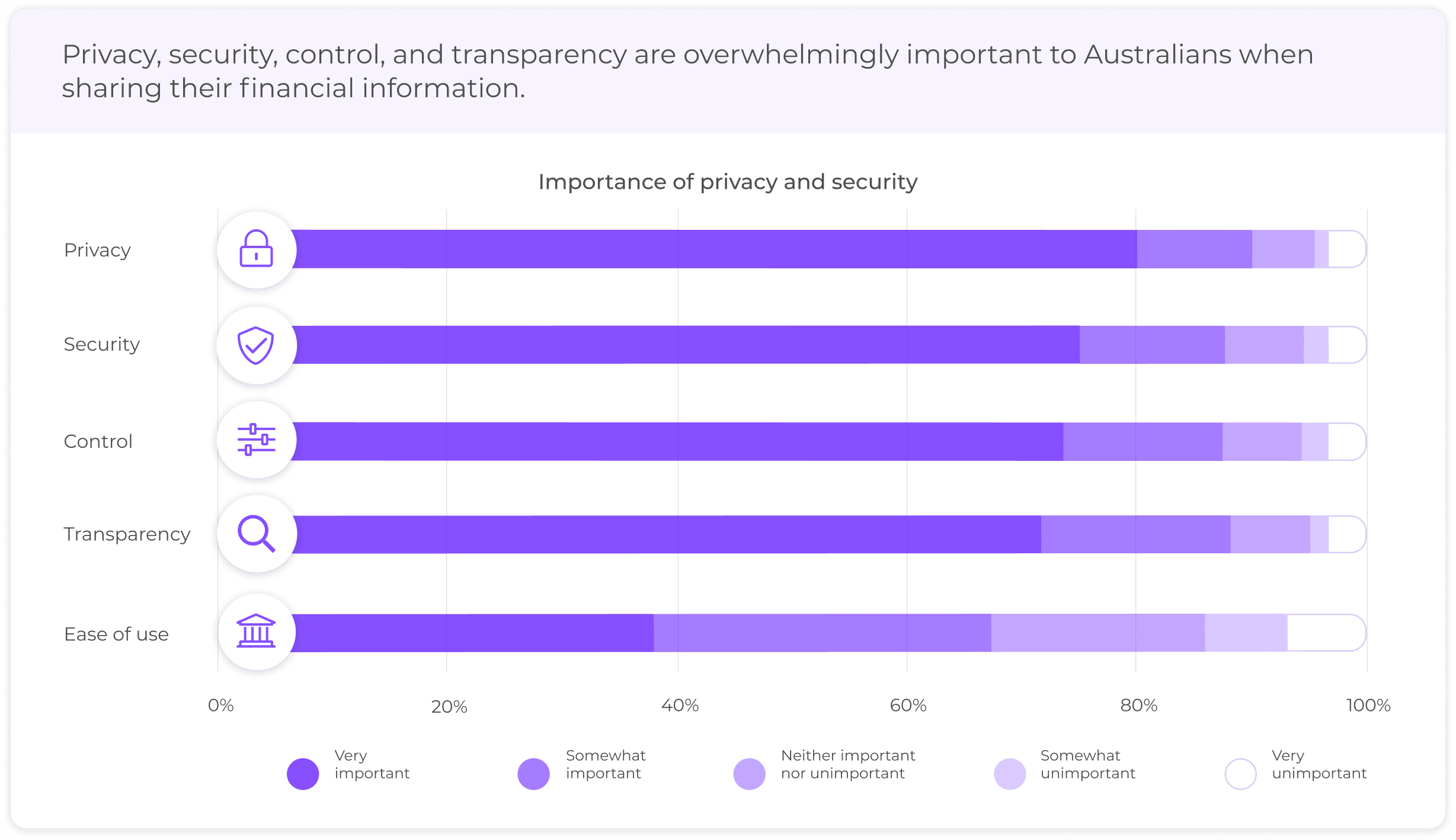

2. Consumers want the network privacy and security Open Banking provides

With the privacy and security risks associated with traditional methods of sharing financial data (such as sharing account credentials or email payslips and bank statements as PDFs), consumers are understandably concerned about the security of their bank accounts, who has their data and what it’s used for. And Australians want to know their data isn’t shared with third parties without their consent.

When asked what’s important when sharing their financial information, Australian consumers’ biggest considerations are:

- 91% Privacy

- 88% Security

- 88% Control

- 88% Transparency.

3. Trust has to be built

Open Banking is inherently a more secure system, protecting consumer privacy and putting them in control of how their data is used. Before Open Banking, there was no reliable way to help consumers decide whether they could trust a business with their financial data – and there hasn’t been a way for businesses to show they’re trustworthy. And when it comes to sharing financial data, trust is an important factor. When asked who they would trust to share financial information with by linking their accounts:

- 55% would trust banks

- 36% would trust utility companies

- 34% would trust brokers/financial advisors

- 27% would trust big technology companies

- 23% would trust fintechs

As a government-regulated regime, Open Banking offers the tools and the stamp of approval that can help build this trust. When consumers use Open Banking to share their data, they can trust your data is more secure, their privacy is protected, and they’re in control (regardless of the business they’re sharing their data with). Open Banking offers the trust layer required to give peace of mind with sharing financial data.

The government established the CDR because it recognised that giving Australians the ability to safely share their data would benefit households as well as the broader economy. Going forward, it’s important to increase awareness of the CDR as the safe way to share data and build trust and confidence in the security and privacy at the core of the system.

Kate O’Rourke (Treasury)

4. Millennials and Gen Z are likely to be the first to get on board

Willingness to engage with Open Banking is very obviously related to age. From the appeal of products and services to trust, the younger demographic is undoubtedly more responsive to the changes Open Banking can bring. And on the flip side, privacy and security concerns are less of a barrier. Two use cases show the biggest generational divide – full financial overview and streamlined mortgage applications.

A full financial overview was found useful by:

- 80% of Gen Z

- 74% of Millennials

- 61% of all Australians.

Streamlined mortgage applications were found useful by:

- 78% of Gen Z

- 72% of Millennials

- 59% of all Australians.

This means that banks wanting to future-proof their profit by engaging younger demographics must exploit all Open Banking opportunities to win over this segment.

Open Banking in action

Beyond consumer attitudes, the biggest indicator of consumer feelings towards Open Banking is their actions – are they using it? And Australian consumers are using it more and more.

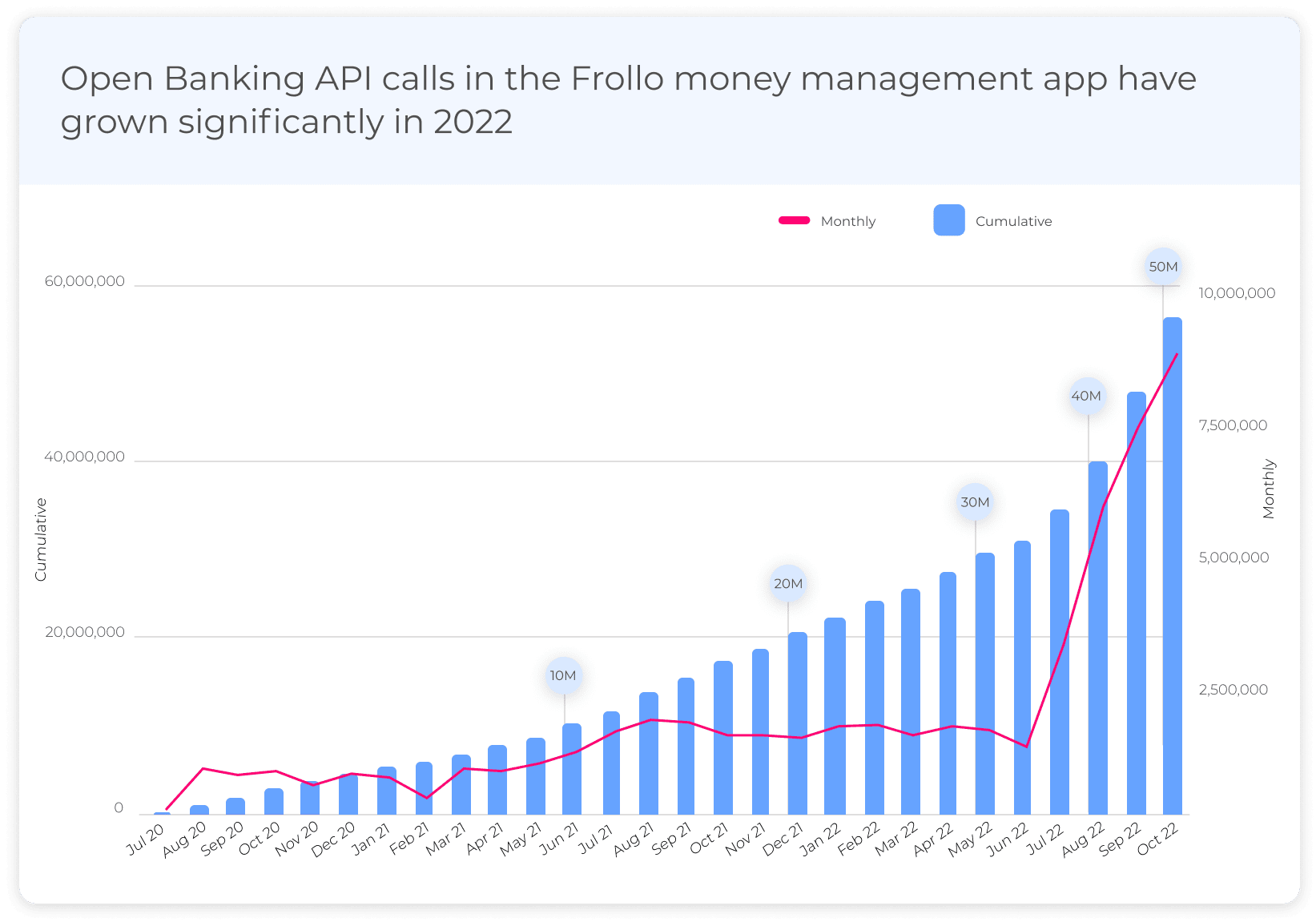

Open Banking usage in the Frollo consumer app has increased fourfold from September 2021 to September 2022. Open Banking API calls have grown steadily, with a notable increase from June 2022, reaching 9 million monthly API calls in October 2022 and adding up to 50 million calls in total since the start of Open Banking.

Overall usage rates will continue to increase as more businesses like Beyond Bank, P&N Bank and Finsure start to use the real-time, reliable financial information to deliver innovative and personalised services. When consumers get a choice to use Open Banking data, their preference is clear: data from the Frollo app shows they are 50% more likely to connect their accounts when they can use Open Banking instead of screen scraping. And with greater product coverage and richer data, more engaging use cases are likely to grow consumer participation further.

This article is part of ‘The State of Open Banking 2023’, an industry report by Open Banking provider Frollo. The report provides a pulse check of the Australian Open Banking industry, interviews with thought leaders and an overview of exciting new use cases.